Las Vegas 2018

Workshop on Making Finance Agile

Have questions about how to make Finance a valued partner to help your DevOps initiatives? Directly hear from the thought leader in making your organization future ready, and a world class FP&A leader who has already shown how leading edge practices can be effectively deployed.

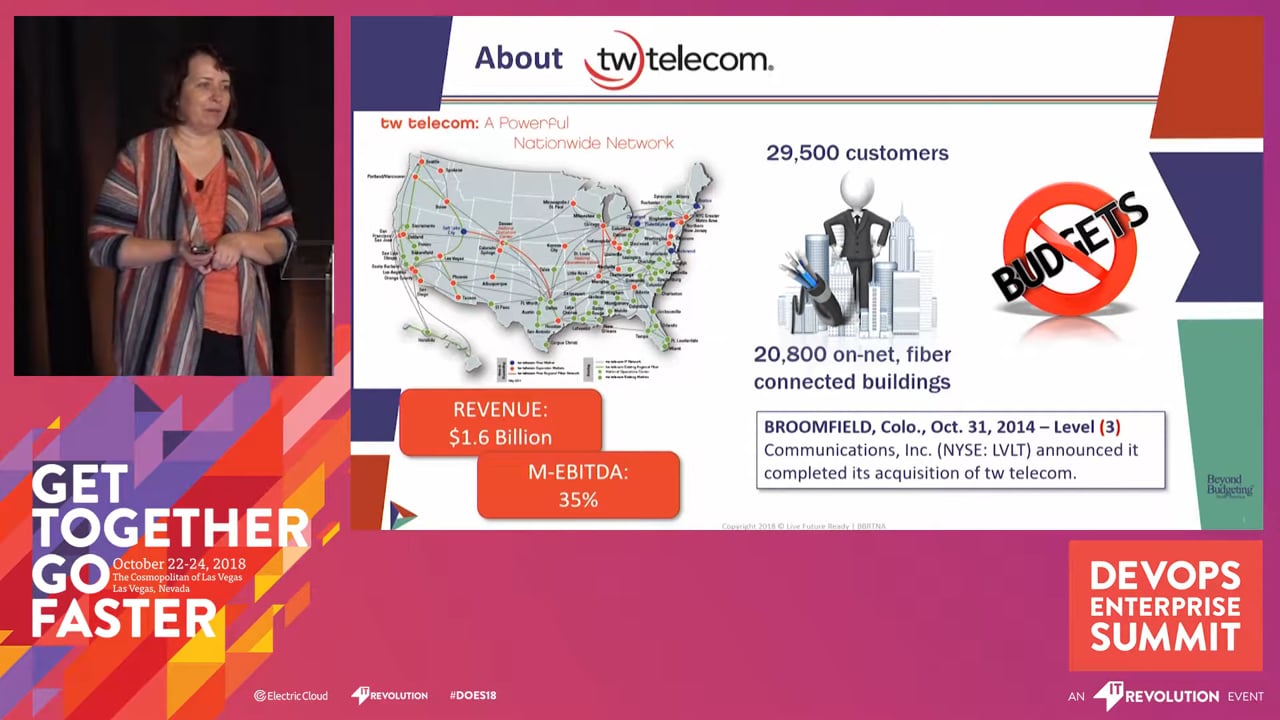

Join Steve Player – Coauthor of Future Ready: How to Master Business Forecasting, and Nevine White – Executive-in-Residence of Live Future Ready (formerly Vice President of Financial Planning and Analysis for publicly-held TW Telecom) as they share how you can create that important cross-functional collaboration that will boost your success. In addition to helping your organization become more agile we are also looking for organizations to further develop the practices and tools needed for collaboration between DevOps, Finance, HR and other disciplines.

Learn how you and your organization can be part of these cross-industry developments.

Steve brings over 30 years of experience in helping organizations implement strategic planning and cost management programs. Steve serves as the North America Program Director for the Beyond Budgeting Round Table (BBRT) and works to implement continuous planning processes. He is also the founder and Managing Director of Beyond EPS Advisors, a Dallas, Texas-based business management consulting firm, and founder of the Activity-Based Management Subject Matter Resource Team (ABM SMART). Previously, Steve was Managing Partner of Arthur Andersen’s Advanced Cost Management Team.

Steve is the co-author/editor of seven books on cost and performance management. He writes a monthly “Finance Transformation” feature for Business Finance Magazine in which he interviews CFOs from leading organizations on innovative finance and planning processes. He also serves on the editorial board for the Journal of Cost Management as well as a resource for various publications including Investor’s Business Daily, Financial World, Global Finance, The Dallas Morning News and Journal of Cost Management.

Steve has served as keynote speaker for many finance organizations and publication events including CFO Magazine, IMA, Business Finance Magazine’s BPM Summit, and several AICPA events. Steve is a CPA and received his BBA degree in Accounting from the University of North Texas.

Nevine White speaks from her experience to educate and enable business leaders in all aspects of strategy and deployment for best-practice, enterprise-wide financial planning, forecasting, and analysis, to drive meaningful changes in planning processes and an empowerment culture that will lead to improved performance.

During her last 10 years leading a corporate FP&A function, Nevine lived the development, implementation, and operation of the most innovative processes in Beyond Budgeting™. This included replacing traditional budgets with rolling forecasts that incorporated multiple levels of data - from detailed analytical projections to macro-economic views - and improved overall forecast accuracy to low, single-digit variances.

Nevine holds a Finance MBA and Bachelor’s degree in Electronics Engineering Technology. She is a former Financial (FP&A) professional with tw telecom (now Level 3 Communications) and has 25+ combined years of experience in the finance and telecommunications arenas.

SP

Steve Player

Owner, The Player Group

NW

Nevine White

Executive in Residence, Beyond Budgeting Round Table North America