London 2020

How a Colossus Took a Duck and Turned it into a Unicorn

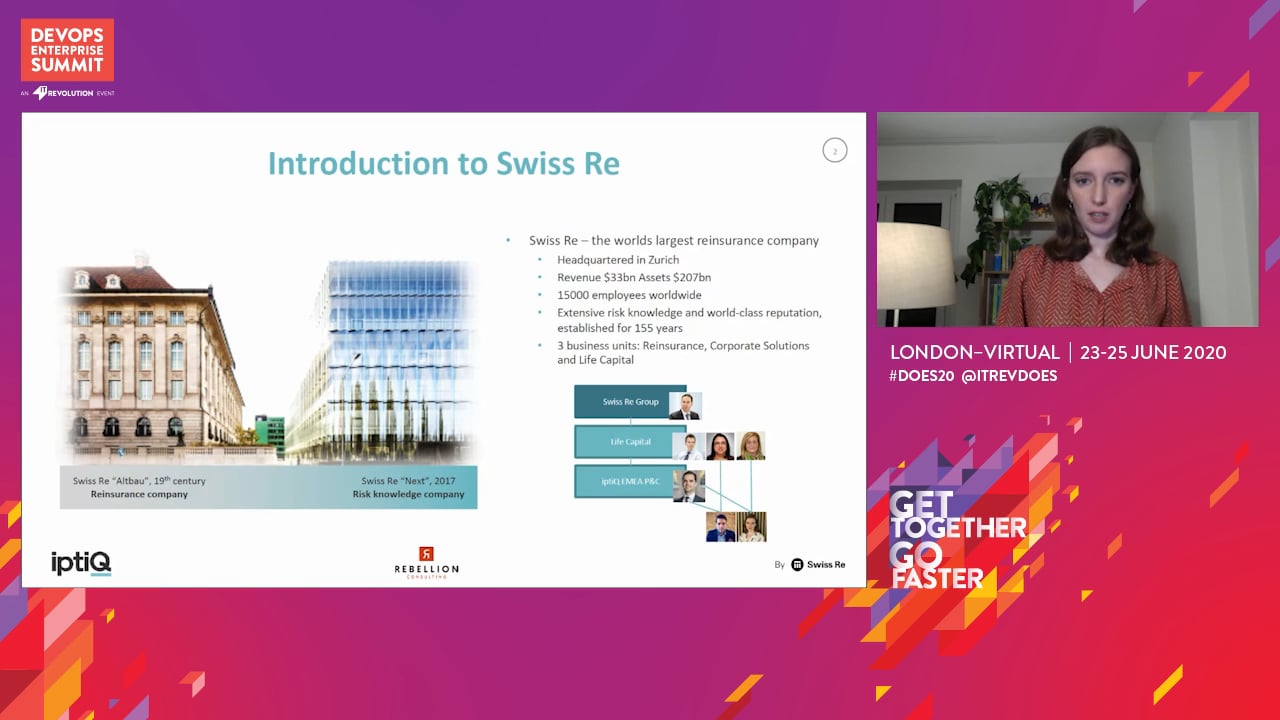

Swiss Re is a Reinsurer with 14,500 employees and an annual revenue circa $34B – their core business for most of their history has been insuring insurers (Reinsurance). In order to diversify, tap into new risk pools and provide a wider range of services, they have created a business unit (Life Capital) to give birth to, nurture and scale B2B2C digital insurance start-ups. In essence, providing digital and operational insurance platform(s) as a service to other large non insurance brands wanting to diversify into insurance but who lack the capability, license and expertise.

This is the story of one of those start-ups: iptiQ P&C EMEA and the first 2 years of its life starting out as a vision and business case all the way through to its launch into 3 markets with its first partners. We want to share our story with you so you can understand the dead-ends and wrong turns, the mistakes and how we ultimately overcame them, the transformation of the company, its culture and ourselves…and how we ‘went native’ and now cannot turn back.

We will tell our story in chapters, each of them describing a stage and key challenge in the journey and how it was ultimately overcome so that we can move onto the next chapter.

The stories' unlikely heroes are Victoria-Head of Compliance and James- Interim Head of Delivery–we will also hear how their lives changed and the impact on them as they progress through this journey. And, of course, we’ll have a few surprises on the way.

VM

Victoria Mayo

Head of Compliance- iptiQ EMEA P&C, Swiss Re

JH

James Head

Founder, Rebellion Consulting